[Adapted from the New Yorker,”Outsmarted”, 2009]

Masters is widely credited as the creator of the credit default swap as a financial instrument.

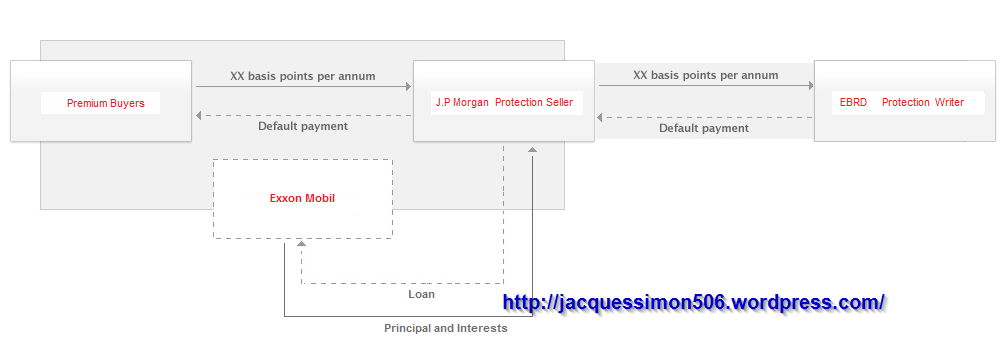

In 1994, Exxon faced the threat of $5 billion in punitive damages for the Exxon Valdez oil spill.

J.P. Morgan had to refinance $4.8 billion credit line and the deal would tie up a lot of reserve cash to provide for the risk of the loans going bad.

However the bank, was reluctant to turn down Exxon which was an old client.

Basel rules required that the banks hold 8% of their capital in reserve against the risk of outstanding loans. That limited the amount of lending bankers could do, the amount of risk they could take on, and therefore the amount of profit they could make.

But, if the risk of the loans could be offloaded, it logically followed that the loans were now “risk-free”; and, if that were the case, what would have been the reserve cash could now be freely loaned out. No need to suck up useful capital.

Blythe Masters, a member of the J. P. Morgan swaps team, pitched the idea of selling the credit risk to the EBRD (European Bank of Reconstruction and Development) to cut the capital which J.P. Morgan was required to hold against Exxon’s default.

So, if Exxon defaulted, the EBRD would be on the hook for it—and, in return for taking on the risk, would receive an annuity (XX basis points) from J. P. Morgan.

At the back-end, J.P. Morgan would finance the strategy by bundling and selling the carry cost of the credit guarantee with the ERBD as a swap market annuity (XX basis points plus (let’s say 100 bps) to Premium buyers.

Layout of the J.P. Morgan-EBRD credit default swap flows on Exxon:

- Exxon would get its credit line and the bank would get to honor its client relationship.

- JP. Morgan had found a way to shift risk off its books while simultaneously generating income from that risk.

- Thus freeing up capital to lend elsewhere.

- The swaps team would earn do its bonus.

.

The arrangement would eventually be streamlined and known as a “credit-default swap.”

* * * * *

It’s Goldman vs JPMorgan As ISDA’s Noble Indecision Roils CDS Market

Some of the world’s biggest investment banks and hedge funds were engaged in a bitter tussle over CDS written against the borrowings of the debt-laden Hong Kong-based commodity trader, Noble Group.

According to the FT, on one hand we have Goldman Sachs, Nomura and hedge funds who bought CDS protection on Noble and would profit if ISDA determined that a CDS trigger event had taken place as they would then be paid off by the sellers of protection; these entities, however, are facing off against JPMorgan, BNP Paribas and other traders who sold the protection. As a result, more so than even the fate of Greek CDS, what happens to Noble, a pure-play corporate name, “is shaping up to be an important test for reforms made to the $10tn CDS market a decade after it was widely blamed for exacerbating the financial crisis.“

The ISDA committee responsible since 2009 for deciding on the status of credit events (is it a default or not) said it was unable to determine if the status of Singapore-listed commodity trader, as reported by the u.s website Zero Hedge, this is a precedent in the 10 trillion dollars credit derivatives market.

Several years ago, the International Swaps and Derivatives Association, or ISDA, lost much of its credibility when during the peak of the Eurozone debt crisis, it first refused to determine that CDS on Greece had been triggered (i.e., that an event of default had taken place) only to eventually concede – following substantial outside pressure – that Greece had, in fact, defaulted (if only on bonds not held by a certain central bank), but not before penning a “petulant” blog post in which it claimed amusingly that the “credit event/DC process is fair, transparent and well-tested”.

The fiasco prompted many, this site included, to dub sovereign Credit Default Swaps as “Schrodinger’s CDS”, contracts which may or may not pay out in case of a default, depending on which way the political winds were blowing at any given time.

Fast forward to today when not only is ISDA in hot water again, but the entire corporate CDS market has been roiled by another indecision by ISDA, which said “it was unable to determine” if Singapore-listed Noble Group, formerly Asia’s largest independent commodity trader was in default or not, creating a vacuum similar to what happened with Greece 5 years ago, and which, according to the FT, has resulted in mass confusion in the corporate bond and CDS market. What is more striking, however, is that this is “the first time ISDA has dismissed a question of default without making a ruling either way.”

“The issue, however, is that without a formal determination by ISDA, Noble CDS remains untriggered and no payouts are actually due.

And while in the case of the Greece CDS trigger, ISDA was facing massive political pressure by the European political (and central bank) class, in the case of Noble the lobbying interests are more nuanced and all reside within Wall Street“.

–

It’s Goldman vs JPMorgan As ISDA’s Noble Indecision Roils CDS Market

Zero Hedge

* * * * *

Banking vs Taking Outright Risk.

In the past I’ve been outspoken about Noble because in my view, it hadn’t the performance nor any adequate financial surface.

At one point in the time, Banks certainly provided liquidity that the trader didn’t qualify for. Bankers were no longer “banking” but taking an outright risk on Noble.

- Partly because Banks had place their confidence into a relational asset, Richard Elman, a very intelligent and an exceptional businessman.

- Richard Elman is like Marshal Suvorov, one of the few generals who had never been defeated…

- Partly because they believed the debris had still liquidation value.

Solvency Problem, not liquidity

“I will make it clear that it is not Liquidity that banks are asking but for more Collateral from Noble starting this year because they also understand that this MTM gain on commodity contracts and derivatives of Noble will unlikely be realized at more than 10% and therefore is not valid collateral for the trader’s working capital borrowing base requirements”.

-Simon Jacques,

Noble Group’s “Collateral Margin Call”, Zero Hedge Jan 2, 2016

“After the quick sale of Noble Agri, Noble’s core business remains its coal & energy – two very depressed commodities for the foreseeable future, and with no cash-flows to pay its debt and a sudden tightening of the credit, the trader is a cancer patient on the forward curve”.

–-Simon Jacques,

Noble Group’s “Margin Call” Part II: The Enron Moment”, Zero Hedge Jan 10, 2016

* * * * *

Noble is a crash-course into the perils of commodity trading & the information asymmetries in the financial markets.

[Largely an excellent summary of Noble, the good counterparty of yestesday that has become a mess out of proportions-what is left is a rotating chair for empty suits draining uncontrolled expenses]:

The burden of Karma is heavy as Noble crosses the gates of death

- Noble presents itself as a $2B net worth company with an $1,45 MtM unaudited Gains on Derivatives company*

- The trader has -$763 million negative OCF with a net debt increased by nearly $1B to $3.81B.

* unaudited.

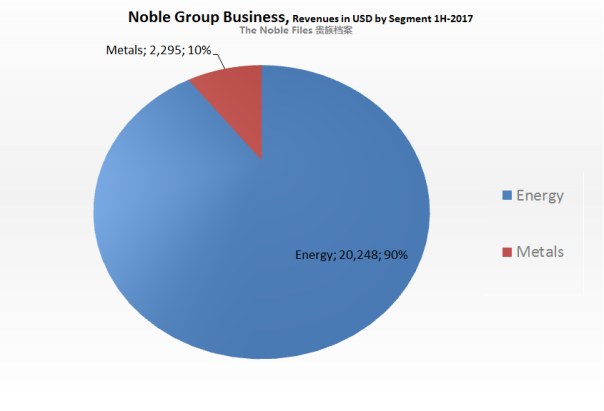

The Energy Segment accounts for 90% of Noble Revenues in 1H-2017.

Noble Group Limited Revenues by Segment, 1H-2017

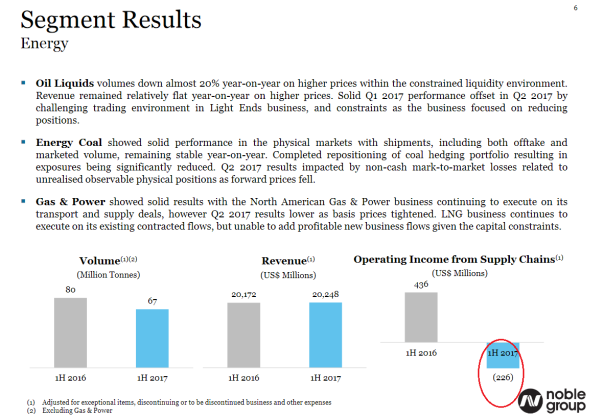

The Energy Segment traded at a loss of $226 million during 1H-2017 (excluding financing costs and salaries).

That’s more than -$1.25 million per business day… Monday to Friday but the business is run smoothly. Of course no.

But in the world of Noble shortlisters rush on a “bargain” 🙂

“Sale of Global Oil Liquids Sales process commenced with shortlist of bidders–bids expected in Q3 2017”

-Strategic Review Update–26 July 2017

Investor Presentation Q2-2017 P.6

Out of Control

The Non-Performance of Global Oil Liquids should not be that shocking knowing the “Book now, think later” at the company.

It lacks the management to impart performance.

Noble had two or three large take-of-pay deals in the U.S but the wind has changed as it always does in the physical energy markets.

The burden of Karma is heavy as Noble crosses the gates of death:

Wendy Ramos is head of chartering in the well-known Stamford trading outfit.

She is referred as the oldest employee. The lawsuit states that Ramos was treated differently than at least five male counterparts in terms of pay, bonus and renumeration.

The hostile work environment includes daily vulgar and disgusting comments from male employees about vaginas, sex, male genitalia, and verbally abusive language using the word ‘f—‘ explicitly. constant abuse.”

A Day on the trade floor.

During 2012-2016, at the office in Stamford, Plaintiff’s seat was next to the gasoline traders which includes video conference cameras connecting with London and Houston offices.

The commentary back and forth on the Stamford desk for everybody within

earshot to hear, frequently became vulgar and disgusting. This created a hostile work environment.It was a constant back and forth across the Stamford desk of sexual innuendo and inappropriate commentary.

HR Policy “D cups”

On or about, 2015, Plaintiff was told that JF and

Mike Kerrigan-Human Resources had a meeting whereby they were discussing restructuring (firing) staff.

Plaintiff was told that JFsaid that they had to keep BS, a young intern, because she was the only “D” cups on the floor, whereby JF and many others laughed about it, including the HR executive.

Incompetence & Arrogance

The Lawsuit alleged that James McNichol and his team lost Noble well over 85 million dollars in the year he left Noble’s employment.

James McNichol came to Noble from Trafigura where he had been accused of being the trader behind a deal that unlawfully disposed of oil waste slops in Nigeria that ultimately caused serious illness of multiple people who came in contact with the disposed slops.

Plaintiff’s first experience with James was during a “Team Building” meeting held in

Barcelona Spain during October 9 11, 2009. Plaintiff was asked to attend and give a presentation relating to the Chartering desk. It was clear from the start of meeting that James had his own agenda for the Oil Group.

Managing the company money.

The entire trading team at the time was in Barcelona where on the first night Plaintiff went to dinner with the group and then to an early night in.

The next day during the Team Building presentations several men were missing. As they showed up in the afternoon hours of the day, the rumor was that the men were not present because they were hung over. As the day progressed, it was said through conversations that these men were out all night at the strip club. After the event, James submitted the “expense” to Ted for reimbursement.

If you run into trouble, just tell a lie to the customer.

On or about, 2009, on information and belief, JM told the London operations manager, ZH, that she needed to convince the inspectors to lie about quality outcomes on cargoes.

James wanted her to do this to make more money. She refused to urge the inspectors to lie and she ultimately quit because she would not do what he asked. During this time at Noble, on information and belief, James proceeded to make questionable trading decisions that were losing the Oil desk millions of dollars.

Book now… think later

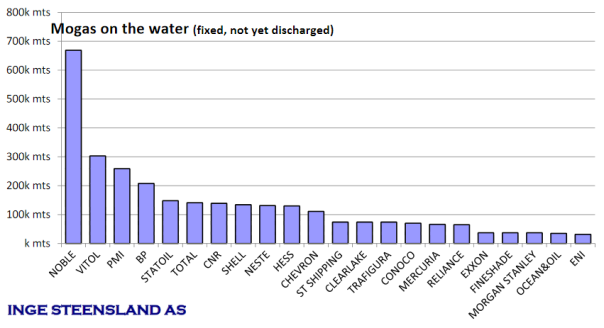

For example, he took on overpriced storage, taking on multiple time charterer ships for Gas and Diesel without consent from Ted.

The spreadsheet below that shows that Noble at that time had taken approximately 670,000 MT for floating storage versus Vitol (the largest trader in theworld) was 2nd with 300,000 MT than the total trading market.

Plaintiff sent this spreadsheet to Ted and asked him to do something about James’ injurious actions.

Not only was he hostile to her, now his behaviors were damaging to the company’s bottom line.

However, nothing was done.

At the end, the unsold cargoes, and empty storage finally caught up to the oil traders, and ultimately J and his team lost Noble well over 85 million dollars in the year he left Noble’s employment.

http://www.tradewindsnews.com/finance/1317292/noble-accused-of-gender-discrimination

*Ramos V Noble Americas Corporation.

Noble did the financial engineering for years and years and then the show–game broke. The typical assumption of a 40% recovery rate may indeed be too optimistic.

* * * * *

CDS spreads are quite intuitive to communicate credit risk. CDS premiums on BBG are in a whole stratosphere since Q1. Noble’s 1-year paper costs 7,500 BPS on the top of a 500 basis points coupon.

The CDS Premium buyer pays a premium and “puts” the bond back in case of default. When the default probability increases, the CDS value rises and the CDS’s Buyer’s Put is in the money- thus he can resell it at a profit.

Smarter traders in Asia have circled around Noble…

* * * * *

GOLDMAN SACHS

Def.: “pure traders are everywhere where there is blood; Argentina, Aluminum warehouses to the finale of a failed trader... “

This is Goldman Sach FICC. They found an opportunity in the radar and the timing, knows the exact definition of the credit event and procedural aspects of ISDA.

BNP PARIBAS

BNP Paribas is different and has a complete different path.

Def.: corporate banker, “small is beautiful”.

They BANK but they aren’t boring bankers. The bank has a world–class franchise in STS (specialized trade solutions), energy and trade finance lending to commodity traders all over the world.

[However as a reminder, the bank had one exposure that has ruined twenty straight years of profits] (see Traders or Commodity Finance Banks Part VII- BNP Negative Skew).

From BNP:

“BNP Paribas has been active in this field for more than 60 years. A true pioneer in commodity trade finance with an unrivalled know-how. Commodities are part of our DNA”.

-“Six reasons why BNP Paribas is a major player in the commodity finance”, BNP Paribas

BNP Paribas Specialized Trade Solutions (STS) offers expertise on commodity and trade / working capital solutions to corporate clients belonging to the commodity ecosystem.

BNP Paribas Specialized Trade Solutions (STS) is dedicated to working capital and trade financing solutions within the commodity value chain. Based in Geneva and Paris, BNP Paribas STS brings commodity expertise in three main sectors: Metals & Mining, Agribusiness, and Energy.

BNP Paribas has what is called “assymetric informations”

To serve BNP Paribas Clients, BNP Paribas STS relies on GTS Group Trade Centers extended network across all geographies. GTS Group Trade Centers are composed of 100 Trade Centers with 300 Trade Specialists in more than 60 countries.

http://www.bnpparibas.ch/en/corporate-institutional/banque-daffaires* * * *

Commodity trading, the dark river flowing inexorably towards an ocean of mysteries should have no secrets for Cargill* or BNP, “the bank accompanying the large traders and corporates”.

[IT BEGS THE QUESTION; How come no one tells BNP Paribas FICC-DO not underwrite CDS protection on the worst counterparty on the planet ? …]

* * * * *

NOBLE CDS THE CONSPIRACY- MATT LEVINE

“Noble Group Ltd. had a credit facility that came due in June, and it asked its banks to extend the maturity for four months until October, and they agreed, averting a default on its debt. Or … not averting a default? What is a default, anyway? Certainly there was no default under the terms of the credit facility, because the banks agreed to extend it.

But what if you had bought credit-default swaps on Noble? Arguably extending the maturity of a credit line, because the company is in financial trouble, is the sort of debt restructuring that CDS are meant to protect against. On the other hand sometimes companies and their banks agree to modify the terms of their debt, and if those agreements are voluntary then what business are they of CDS holders?

In any case, people who bought Noble CDS think that there was a default, and people who sold Noble CDS think that there was no default, and so they went to the International Swaps and Derivatives Association’s Determinations Committee to ask for a ruling. The committee punted, deciding “that it currently does not have sufficient information that is public or that can be made public to determine the Restructuring Credit Event DC Question one way or the other,” in part because no one sent it a copy of the amended credit facility. This is not great:

In the absence of a ruling from ISDA, banks and funds that have bought or sold Noble CDS are essentially flying blind, with no precedent to follow, except how the market operated pre-2009.

“It’s like the whole last 10 years of market development have been put to one side,” said Nigel Dickinson, a derivatives lawyer at Norton Rose Fulbright.

The ISDA Determinations Committee was asked to try again. The ISDA Credit Derivatives Definitions define a “Restructuring” credit event, which triggers CDS, to include “a postponment or other deferral” of payments in a debt instrument “in a form that binds all holders” of that instrument, unless it “does not directly or indirectly result from a deterioration in the creditworthiness or financial condition of the” issuer. Did Noble’s extension bind all holders of its credit facility, and result from a deterioration in its creditworthiness? I suppose you’d want to read the documents to find out”.

“The incentives of CDS “. This is where it becomes tricky…

[We have talked a few times about the incentives of CDS: If you have bought CDS on a company, you want it to default, and you might even be willing to offer it attractive financing in exchange for concocting a brief default that triggers CDS].

[If you have sold CDS on a company, you want it not to default, and you might even be willing to offer it attractive financing in exchange for delaying a default. But you have to know which is which! If you agree to extend a maturity date in order to avoid a default, you don’t want that extension to end up being a default itself].

https://www.bloomberg.com/view/articles/2017-08-28/tender-offers-and-ceo-searches

Another drop of enigma, it seems, in a river of obscurities.

_______________

*for further references; https://jacquessimon506.wordpress.com/page/3/?s=cargill&submit=Search

Exclusive advisor to leading energy marketers and producers with energy merchant assets, complex risk fundamentals applied to a macro view on prices, spreads and non-linear dynamics, I impart the knowledge and business skill sets necessary for the professional staff to function effectively.

Simon Jacques is a certified Energy Risk Professional, as distinguished by the prestigious Global Association of Risk Professionals. His Transactional & Operations expertise in commodities is based on hundreds of engagements with some of the world’s leading houses and banks in energy and agricultural commodities at Commodity Merchant Trading and Shipping Advisory Services, the international commodity merchant trading consultancy dedicated to help a clientele comprised of traders/merchants and banks to achieve world-class competency in commodity trading and trade finance.

Navigating the commodities markets with Freight and Spreads © 2017